![]() Call us now:

Call us now:

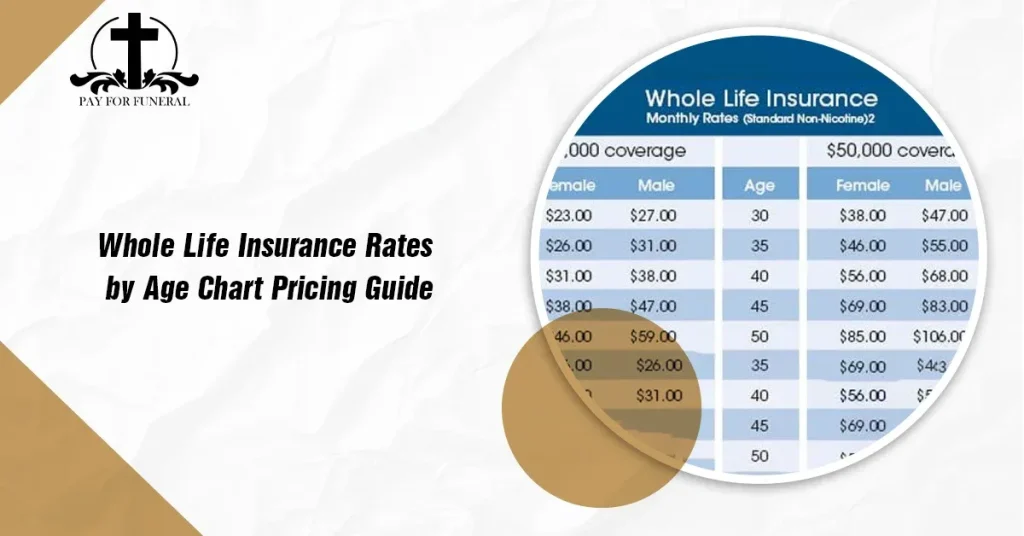

You will get funeral protection with low monthly premiums that will fit your budget and personal needs.

Your family receives the money quickly to cover the funeral and burial expenses without any wait.

You can apply easily by answering a few health questions; there is no need to give a medical exam or any doctor visit to apply.

The plans include cash insurance benefits plus family support services to make funeral planning easy and stress-free.

Secure today’s prices and protect your family from future financial stress by planning your funeral in advance.

You have to choose the payment schedule that works best for you. If you want it to pay monthly, quarterly, or yearly, it's all your choice.